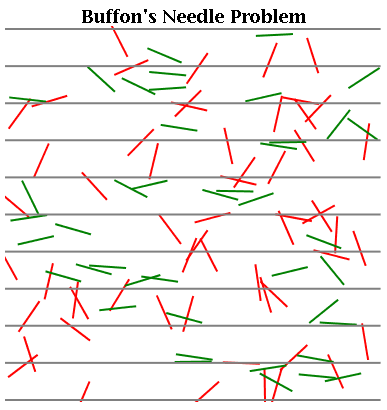

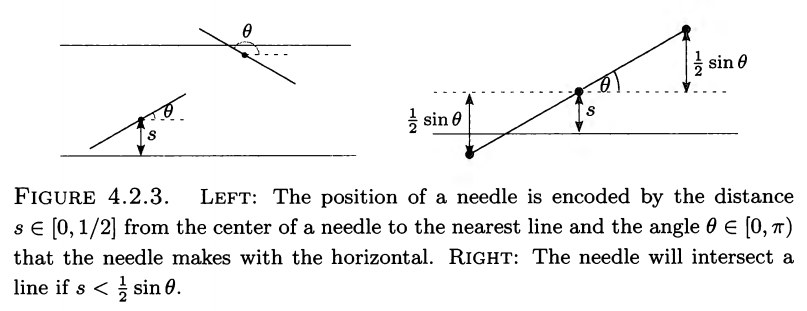

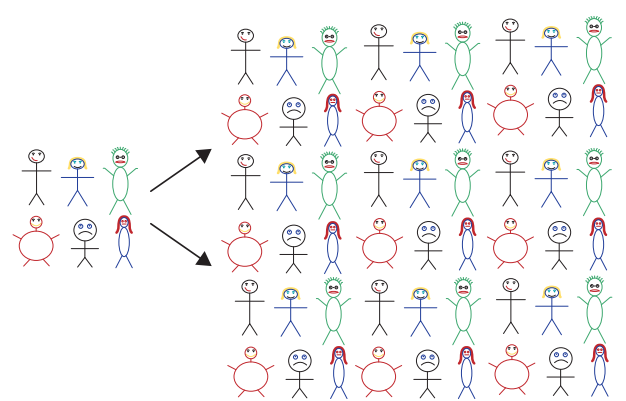

class: center, middle, inverse, title-slide .title[ # Lecture 11: Applications of Simulation ] .author[ ### Robin Liu ] .institute[ ### UCSB ] .date[ ### 2022-07-11 ] --- class: inverse, middle, center # Monte Carlo Methods --- # Monte Carlo Methods .center[] Simulation is a very powerful tool *Monte Carlo* methods are a class of techniques that introduce randomness to solve non-random problems. --- # Approximating `\(\pi\)` Suppose we knew that the area of the unit circle is `\(\pi\)`. However, we do not know the numerical value of `\(\pi\)`. <img src="Lec11_files/figure-html/unnamed-chunk-1-1.png" style="display: block; margin: auto;" /> -- **Idea:** Sample points in this figure uniformly. The proportion of points that fall within the circle should approximate the ratio of the area of the circle to that of the surrounding square, which has area 4. --- # Approximating `\(\pi\)` <img src="Lec11_files/figure-html/unnamed-chunk-2-1.png" style="display: block; margin: auto;" /> ``` ## [1] "8 out of 10 points" ``` `\(\frac{8}{10} \approx \frac{\pi}{4} \implies \pi \approx 3.2\)` --- # Approximating `\(\pi\)` <img src="Lec11_files/figure-html/unnamed-chunk-3-1.png" style="display: block; margin: auto;" /> ``` ## [1] "88 out of 100 points" ``` ``` ## [1] "3.52" ``` --- # Buffon's Needle Throw a length 1 needle onto a sheet of paper with lines length 1 apart. What is the probability the needle crosses the line? .center[] --- # Buffon's Needle Throw a length 1 needle onto a sheet of paper with lines length 1 apart. What is the probability the needle crosses the line? .center[] [src](https://matrixeditions.com/5thUnifiedApproach.html) -- `\(\mathbb{P}(\text{needle crosses line}) = \mathbb{P}(s < \frac{1}{2}\sin\theta)\)` --- # Buffon's Needle `\(\mathbb{P}(\text{needle crosses line}) = \mathbb{P}(s < \frac{1}{2}\sin\theta)\)` Assume `\(s \sim \operatorname{Unif}(0, 1/2)\)`, `\(\theta \sim \operatorname{Unif}(0, \pi)\)`. .center[] --- # Buffon's Needle Assume `\(s \sim \operatorname{Unif}(0, 1/2)\)`, `\(\theta \sim \operatorname{Unif}(0, \pi)\)`. The pdf of `\(\operatorname{Unif}(a,b)\)` is `\(\frac{1}{b-a}\)`. Hence the pdf of `\((s, \theta)\)` is `$$f(s,\theta) = \frac{1}{1/2}\cdot \frac{1}{\pi} = \frac{2}{\pi},\; s \in (0, 1/2),\, \theta\in(0,\pi)$$` -- This yields `\begin{align} \mathbb{P}(\text{needle crosses line}) &= \mathbb{P}\left(s < \frac{1}{2}\sin\theta\right) \\ &= \int_0^\pi \int_0^{\frac{1}{2}\sin\theta} f(s,\theta)\mathrm{d}s\, \mathrm{d}\theta \\ &= \frac{2}{\pi}\int_0^\pi \int_0^{\frac{1}{2}\sin\theta} \mathrm{d}s\, \mathrm{d}\theta \\ &= \frac{2}{\pi}\int_0^\pi {\frac{1}{2}\sin\theta}\, \mathrm{d}\theta = \frac{2}{\pi} \approx 0.637 \end{align}` --- # Buffon's Needle .center[] `\(\mathbb{P}(\text{needle crosses line}) = \mathbb{P}(s < \frac{1}{2}\sin\theta)\)` --- # Buffon's Needle `\(\mathbb{P}(\text{needle crosses line}) = \mathbb{P}(s < \frac{1}{2}\sin\theta) = \frac{2}{\pi}\)` ```r set.seed(100) nrep <- 1000 s <- runif(nrep, 0, 1/2) theta <- runif(nrep, 0, pi) r <- s < sin(theta) / 2 plot(1:nrep, cumsum(r)/1:nrep, type = "l") abline(h = 2/pi, col = "red") ``` --- # Buffon's Needle `\(\mathbb{P}(\text{needle crosses line}) = \frac{2}{\pi}\)` <img src="Lec11_files/figure-html/unnamed-chunk-6-1.png" style="display: block; margin: auto;" /> [Demo](https://www.ventrella.com/Buffon/) --- # Monte Carlo Integration Use simulation to compute the following: `$$\int_0^{10} x^2\, \mathrm{d}x$$` -- **Idea:** Express the integral as the *expectation* of a certain random variable. Let `\(X\sim \operatorname{Unif}(0, 10)\)` with pdf `\(f_X(x) = \frac{1}{10}\)` for `\(0< x < 10\)`. `\begin{align*} \int_0^{10} x^2\, \mathrm{d}x &= \int_0^{10} 10x^2 \frac{1}{10}\mathrm{d}x \\ &= \int_0^{10} 10x^2 f_X(x)\mathrm{d}x = \mathbb{E}(10X^2). \end{align*}` --- # Monte Carlo Integration Approximate `\(\mathbb{E}(10X^2)\)` where `\(X \sim \operatorname{Unif}(0, 10)\)` ```r set.seed(100) nrep <- 10000 x <- runif(nrep, min = 0, max = 10) mean(10 * x^2) ``` ``` ## [1] 333.0308 ``` `$$\int_0^{10} x^2 \mathrm{d} x = \frac{x^3}{3}\bigg\lvert^{10}_0 = 10^3/3 \approx 333.33$$` --- # Monte Carlo Integration Define `\(f(x) = \sqrt{x^3 + \sqrt{x}} - x^2 \sin(4x)\)`. ```r f <- function(x) { sqrt(x^3 + sqrt(x)) - x^2 * sin(4 * x) } curve(f, from = 0, to = pi) ``` <img src="Lec11_files/figure-html/unnamed-chunk-8-1.png" style="display: block; margin: auto;" /> Compute `\(\int_0^\pi f(x) \mathrm{d}x\)`. --- # Monte Carlo Integration `\(f(x) = \sqrt{x^3 + \sqrt{x}} - x^2 \sin(4x)\)`. Our domain of integration is from `\(0\)` to `\(\pi\)`. We can sample uniformly from `\(X\sim \operatorname{Unif}(0, \pi)\)` with pdf `\(g_X(x) = 1/\pi\)`. `\begin{align*} \int_0^\pi f(x) \mathrm{d}x &= \int_0^\pi \pi f(x) \cdot \frac{1}{\pi}\mathrm{d}x \\ &= \int_0^\pi \pi f(x) \cdot g_X(x) \mathrm{d}x \\ &= \mathbb{E}(\pi f(X)) \end{align*}` --- # Monte Carlo Integration `\(\int_0^\pi f(x) = \mathbb{E}\left(\pi f(X)\right)\)`, `\(X\sim \operatorname{Unif}(0, \pi)\)`. ```r f <- function(x) { sqrt(x^3 + sqrt(x)) - x^2 * sin(4 * x) } nrep <- 1600 x <- runif(nrep, min = 0, max = pi) mean(pi * f(x)) ``` ``` ## [1] 10.558 ``` --- # Monte Carlo Integration ```r f <- function(x) { sqrt(x^3 + sqrt(x)) - x^2 * sin(4 * x) } nrep <- 1600 x <- runif(nrep, min = 0, max = pi) y <- cumsum(pi * f(x)) / 1:nrep plot(1:nrep, y, type = "l") abline(h = pi^2/4 + 0.4*(pi^(5/4)*sqrt(1+pi^(5/2))+asinh(pi^(5/4))), col = "red") ``` <img src="Lec11_files/figure-html/unnamed-chunk-10-1.png" style="display: block; margin: auto;" /> --- class: inverse, middle, center # The Bootstrap --- # Bootstrap The **bootstrap** is a widely applicable and extremely powerful method that is used to *quantify uncertainty* of statistical estimators. The idea is, from a provided sample, draw random samples from it *with replacement*. -- The `flights` tibble contains **all** flights that departed NYC in 2013. ```r library(nycflights13) library(tidyverse) flights ``` ``` ## # A tibble: 336,776 x 19 ## year month day dep_time sched_dep_time dep_delay arr_time sched_arr_time ## <int> <int> <int> <int> <int> <dbl> <int> <int> ## 1 2013 1 1 517 515 2 830 819 ## 2 2013 1 1 533 529 4 850 830 ## 3 2013 1 1 542 540 2 923 850 ## 4 2013 1 1 544 545 -1 1004 1022 ## 5 2013 1 1 554 600 -6 812 837 ## 6 2013 1 1 554 558 -4 740 728 ## 7 2013 1 1 555 600 -5 913 854 ## 8 2013 1 1 557 600 -3 709 723 ## 9 2013 1 1 557 600 -3 838 846 ## 10 2013 1 1 558 600 -2 753 745 ## # ... with 336,766 more rows, and 11 more variables: arr_delay <dbl>, ## # carrier <chr>, flight <int>, tailnum <chr>, origin <chr>, dest <chr>, ## # air_time <dbl>, distance <dbl>, hour <dbl>, minute <dbl>, time_hour <dttm> ``` --- # Bootstrap Since it contains all flights, we know the *true mean* of the duration of the flights, in minutes: ```r (true_mean <- mean(flights$air_time, na.rm = T)) ``` ``` ## [1] 150.6865 ``` We need `na.rm = T` since the data has *missing (NA) values*. We can ignore these. -- Let's pretend we did not have data on all of the flights. Instead, we observe a *random sample* of flights from NYC in 2013. ```r set.seed(101) flights_smpl <- flights |> select(dep_time, arr_time, air_time, distance) |> slice_sample(n = 50) ``` --- # Bootstrap `dplyr::slice_sample(n = 50)` gave us a random sample of 50 of flights. ```r flights_smpl ``` ``` ## # A tibble: 50 x 4 ## dep_time arr_time air_time distance ## <int> <int> <dbl> <dbl> ## 1 819 1103 312 2446 ## 2 1238 1342 47 266 ## 3 1953 2141 62 419 ## 4 608 752 73 419 ## 5 1653 1815 108 765 ## 6 1813 2026 92 569 ## 7 1740 2054 352 2586 ## 8 834 1031 80 479 ## 9 1014 1219 109 708 ## 10 1741 2024 135 944 ## # ... with 40 more rows ``` --- # Bootstrap Suppose we want to estimate the average `air_time` from the random sample. What is a good estimate? -- Most obvious: use our sample mean, `\(\bar x\)`. ```r (xbar <- mean(flights_smpl$air_time, na.rm = T)) ``` ``` ## [1] 147.26 ``` <img src="Lec11_files/figure-html/unnamed-chunk-16-1.png" style="display: block; margin: auto;" /> --- # Bootstrap `\(\bar x\)` appears to be a good estimate. But how good? -- Remember we calculated `\(\bar x\)` from one random sample of size 50. If we collect a different random sample, we will get a different value of `\(\bar x\)`. `\(\bar x\)` is an observation of a *random variable* `\(\bar X\)`. -- One way to assess our estimate is to ask the following: what is the *standard deviation* of `\(\bar X\)`? -- Standard deviation measures how spread out `\(\bar X\)` can be. Large standard deviation means less accurate. -- Standard deviation of `\(\bar X\)` is also called the *standard error*. --- # Bootstrap I plot additional sample means from samples of size 50. Our estimate is different each time. <img src="Lec11_files/figure-html/unnamed-chunk-17-1.png" style="display: block; margin: auto;" /> --- # Bootstrap Here I plot four estimates of the true mean from a "worse" estimator (using a small sample size). <img src="Lec11_files/figure-html/unnamed-chunk-18-1.png" style="display: block; margin: auto;" /> --- # Bootstrap We want to estimate the standard deviation of `\(\bar X\)`. ### Idea - Take 1,000 random samples of size 50 from the *population* of flights. - Compute 1,000 sample means - Compute the *sample standard deviation* of the 1,000 sample means. -- ### Problem We assumed we only see *one sample* of size 50. We cannot keep taking random samples if we do not know the population! -- ### Solution We take samples of size 50 *from our original sample of size 50*. This sampling is done **with replacement**. --- # Bootstrap .center[] Using a sample to represent a population. [credit](https://www.lock5stat.com/) --- # Bootstrap <img src="Lec11_files/figure-html/unnamed-chunk-19-1.png" style="display: block; margin: auto;" /> This is a **bootstrap confidence interval**. We only observed a single sample whose sample mean is in blue. But we are "confident" that the true mean is within the interval. --- # Bootstrap Regression ### Who will be elected president? **Bread and peace model:** Good times predict the incumbent to win. ```r (hibbs <- as_tibble(read.csv("Lec11_files/hibbs.dat", sep = ""))) ``` ``` ## # A tibble: 16 x 5 ## year growth vote inc_party_candidate other_candidate ## <int> <dbl> <dbl> <chr> <chr> ## 1 1952 2.4 44.6 Stevenson Eisenhower ## 2 1956 2.89 57.8 Eisenhower Stevenson ## 3 1960 0.85 49.9 Nixon Kennedy ## 4 1964 4.21 61.3 Johnson Goldwater ## 5 1968 3.02 49.6 Humphrey Nixon ## 6 1972 3.62 61.8 Nixon McGovern ## 7 1976 1.08 49.0 Ford Carter ## 8 1980 -0.39 44.7 Carter Reagan ## 9 1984 3.86 59.2 Reagan Mondale ## 10 1988 2.27 53.9 Bush, Sr. Dukakis ## 11 1992 0.38 46.6 Bush, Sr. Clinton ## 12 1996 1.04 54.7 Clinton Dole ## 13 2000 2.36 50.3 Gore Bush, Jr. ## 14 2004 1.72 51.2 Bush, Jr. Kerry ## 15 2008 0.1 46.3 McCain Obama ## 16 2012 0.95 52 Obama Romney ``` --- # Bootstrap Regression ```r lm_hibbs <- lm(vote ~ growth, data = hibbs) coef(lm_hibbs) ``` ``` ## (Intercept) growth ## 46.247648 3.060528 ``` <img src="Lec11_files/figure-html/unnamed-chunk-22-1.png" style="display: block; margin: auto;" /> --- # Bootstrap Regression Assess the quality of this model using bootstrap samples. <img src="Lec11_files/figure-html/unnamed-chunk-23-1.png" style="display: block; margin: auto;" /> -- We see there is more uncertainty where there is less data.